Interest Matrix

Within the framework of the “Readers Club” project, the VIEW newspaper presents the text of Alexander Polygalov about why the Ukrainian scenario is designed to oust Russia from the European energy market.

Within the framework of the “Readers Club” project, the VIEW newspaper presents the text of Alexander Polygalov about why the Ukrainian scenario is designed to oust Russia from the European energy market.I am not a supporter of conspiracy theories and do not consider that all those events that are happening now in Ukraine and around Ukraine are a step-by-step realization of someone’s single, carefully calculated idea, all the details of which are interconnected and programmed.

This is also because for the existence of such a plan, the system of management and decision-making in the West would have to be a kind of hierarchically built web, all the threads of which converge in a single center.

The world's largest consumers and exporters, as well as the countries with the largest gas reserves

This situation seems to me impossible for a number of reasons, the main of which is as follows: the modern Western world is so complex that such a spider structure, had it actually had place, would have been completely uncontrollable.

I am rather inclined to share the point of view according to which, in the person of the modern West, we are dealing rather with a matrix (network) structure that does not have a single center, but there are many interrelated interest groups.

These groups consist of politicians from various countries and various parties, lobbyists from various sectors of the economy (including military-industrial complex lobbyists), various NGOs, financiers associated with various financial institutions, and the like.

Each such group has several areas of interest. In all its “own” directions, it interacts with other groups within the same matrix or network structure, and the list of “contacts” in one direction will, as a rule, be fundamentally different from the list of “contacts” in another direction.

In this connection, in my opinion, several such groups are interested in Ukraine at once, each of which has its own specific interests.

In the future, I just venture to state my vision regarding some of these narrow aspects of the current situation in Ukraine, which today seem to me the most important and significant for Russia: from the textbook expression of the late Felix Edmundovich, today Russia (both the government and society) in relation to Ukraine simply must remain "with a cold head, a warm heart and clean hands."

The point is not at all that I am impressed by the methods of Comrade Dzerzhinsky during the civil war, which he covered with this famous phrase, no. The fact is that the literal, downright painful following of the stated maxim for Russia today is a matter of winning in the Ukrainian party.

In a party where the stake has long been not someone’s prestige or even the beautiful constructions of the “united Russian world”, but the lives of Russians in Ukraine, the financial and economic well-being of Russia itself in the short term, as well as its military security in the longer term .

Today the price of a mistake and the price of criminal indifference are incredibly high. And it is precisely on this thin thread - between common sense and not indifference - that we all have to go through without falling and not getting dirty. Within each of the mentioned narrow aspects, each of which can be very little associated with its neighbors.

Part I. The gas issue. Cold head

The dear Anatoly El Murid described quite succinctly what will happen in the short term with Ukraine’s gas debt to Russia, as well as with gas supplies from Russia to Ukraine and to Europe.

If we briefly describe the sequence of future events, it will look like this: Ukraine continues not to pay for consumed Russian gas, in response to this, Russia has the opportunity to choose from the following options.

a) Shut off gas supplies to Ukraine, leaving the transit of gas through Ukraine to Europe. Ukraine steals European supplies, Europe loses gas and a Russian-European gas crisis arises along the lines of the 2008 – 2009 conflict.

And the conflict showed that the European bureaucracy blames Russia for any gas supply disruptions, without bothering with the proceedings, who exactly stole the European gas, and the European public is inclined to accept this information as true.

b) Shut down both gas supplies to Ukraine and gas transit to Europe through Ukraine. The situation arises absolutely similar, with the amendment that now the hysterical accusations of Euro-Atlantists of “energy strangulation of Europe” will become even more difficult to refute, because instead of stealing gas from Ukraine, we will only have to reason that we are forced to stop / does not pay for gas.

c) Do not block any gas supplies to Ukraine or transit to Europe through Ukraine. This means that, in fact, we undertake the financing of the illegitimate Russophobic regime in Ukraine, which is leading a frenzied information war against us.

In addition to the obvious image losses, this option also implies direct financial losses for Gazprom and Russia as a whole. Moreover, it should be understood that regardless of the further development of events in Ukraine, no one will return Ukrainian debt for gas: neither Ukraine, nor Europe, nor the IMF. This is a direct and irrecoverable loss.

Thus, in the short term, any of the options for us is negative, and we will have to choose in just a month.

Interesting position of the IMF, in which the main shareholder is the United States and who not so long ago explicitly stated that its financial assistance to Ukraine related to the payment of gas debt, preserves the discount in 100 dollars per thousand cubic meters, canceled by Russia after the annexation of the Crimea, and that financial assistance to Ukraine as a whole will be provided only after it resolves the “Eastern Question”.

If this is not an action aimed at finally making the knot of contradictions between Russia and Ukraine Gordian (which, as you know, can be cut, but not untied), then I do not even know what it is.

But let's see what are the possible long-term consequences of the still-hypothetical Russian-Ukrainian gas crisis, the short-term prerequisites for the occurrence of which were just described.

My hypothesis, which I will try to justify later, is as follows. The crisis in Ukraine today is trying to take advantage of US energy company lobbyists and related officials of the US administration in order to eventually enter the European energy market, if possible, pushing competitors out of it - and, above all, Russia.

US gas market by 2014: export, import and domestic prices

Today, few people in Russia are aware of the global changes that have taken place in the US gas market over the past five to seven years, and even more broadly on the gas market in North America.

Today, the North American natural gas market remains the third largest supply market in the world (after the European and Asian-Pacific markets, the APR).

Until recently, the bulk of the gas trade in North America accounted for pipeline supplies from Canada to the United States. However, with the growth of shale gas production in the United States there have been significant changes in both the volume of gas supplies and in their direction.

As of now, the US still imports about 85 – 90 billion cubic meters. meters of gas per year, mainly through pipelines from Canada (80 – 85 billion cubic meters). At the same time, the paradox of the situation is that in recent years the USA - due to the growth of shale gas production - has been steadily increasing its gas exports to the same Canada.

Thus, in recent years, such exports amount to about 30 billion cubic meters. m of gas per year. And the total exports from the United States, for example, in 2012, have already reached 46 billion cubic meters. meters per year, that is, amounted to about half of gas imports to the United States.

This state of affairs arose for two main reasons. First of all, it’s about the underdevelopment of transport infrastructure in Canada itself. Basically, Canadian transportation infrastructure consists of pipelines from specific fields in the United States.

The construction of these pipelines, as a rule, was once financed by energy transnational corporations (TNCs) based in the same United States. It is clear that these corporations had no desire to develop the transport infrastructure of Canada itself. Because of this, it is more profitable today to deliver gas to certain regions of Canada from the USA than from Canada itself.

I note that this situation is a private illustration of the fact that Canada today is nothing more than a raw material appendage of the United States, and not at all an independent player.

For the same reason, the US continues to import gas from Canada, because pipeline gas is still one of the most profitable fuels. It makes a profit even at the current (due to an excess of gas in the domestic market) low prices in the US market - about 150 dollars per thousand cubic meters.

And despite the fact that in 2012, the price dropped to 100 dollars per thousand cubic meters. Pipelines have already been built, money has already been invested. In fact, this is the second reason for this paradoxical situation in the North American gas market.

On the one hand, Canadians (as well as the same American TNCs, which largely own gas fields in Canada), have no particular place to go except supplying natural gas to the United States, since no one else will build other pipelines to them today.

Americans, on the other hand, also have nowhere to go except to buy Canadian pipeline gas, and at very low prices due to an excess of gas in the US market, because otherwise billions of dollars invested in the construction of pipelines will be thrown to the wind.

Actually, “there is nowhere to go” is a relative concept: the gas consumers themselves are very satisfied with this situation. What, however, can not be said about energy companies.

To make it clear the value of the discount that the American industry is receiving today thanks to cheap natural gas, it is convenient to compare the cost of various energy carriers through the cost of a unit of energy contained in them. Usually, the British thermal unit, or BTU (in BTU, in English, is used for these purposes).

Thus, one barrel of light oil (such as European Brent or American WTI) contains approximately 5,825 million BTU, and one thousand cubic meters of natural gas contains approximately 35,8 million BTU.

So, according to the IMF, the cost of energy derived from oil in the OECD countries in 2012 averaged 17,5 dollars per million BTUs. At the same time, the cost of liquefied natural gas (LNG) in the APR countries (this is the main region of consumption of LNG), more precisely, in Japan, amounted to 16,6 dollars per million Btu, the cost of natural gas in Europe averaged 11,5 dollars per million BTU, and the internal cost of the pipeline gas in the US was 2,8 dollars per million btu.

In 2013, it rose to 3,8 dollars per million BTUs, which is still several times less than the cost of gas in Europe, not to mention liquefied natural gas in the APR. Remember these numbers, they later will be very useful to us.

So, we have the following facts. The United States today is actively reducing imports of natural gas, and vice versa, increasing exports. At the same time, American energy TNCs cannot completely abandon imports, since with this approach their investments in US-Canadian pipelines are completely lost. At the same time, due to the excess gas in the US domestic market, the price there is several times lower than the price of natural gas in other regions of the world.

Shale revolution and liquefied natural gas

The situation described above was the result of the so-called shale revolution and a sharp increase in natural gas production in the United States. This has already been said a great many times, so now I will focus only on two rather important points of this phenomenon.

The main routes of Russian gas supplies to Europe

First, shale gas - compared to ordinary natural gas, which can be transported through pipelines - contains certain impurities that make it impossible for its regular pipeline transportation over long distances.

Shale gas must either be consumed in the immediate vicinity of the extraction site, or must be cleaned of impurities. But in the latter case, it becomes more profitable not to pump clean shale gas into pipelines, but to turn it into liquefied.

Secondly, in the extraction of shale gas, whose content per unit area of the field is on average very small, the development of large areas at each field is required immediately. It is required to drill a large number of wells per unit area, and the flow rate of each of them drops sharply after a relatively short operating time.

Thus, these two reasons cause, first, the need for high initial investment per unit of shale gas produced, and second, the need for high operating costs for cleaning and transporting such gas.

Even in the USA, where the mining and transport infrastructure has been around for several years, the cost of shale gas production in 2012 was estimated at 150 dollars per thousand cubic meters, that is, for example, significantly higher than the domestic price of natural gas pipelines in the United States itself.

However, opinions have also been repeatedly expressed that the actual cost of shale gas production is much higher and amounts to about 200 – 300 dollars per thousand cubic meters.

But if the cost of shale gas production exceeds current domestic prices in the United States and if shale gas still requires measures to clean impurities before pipeline transportation, would it not be logical to liquefy a portion of shale gas and export it outside the US?

Moreover, the cost of liquefied gas, as shown above, is significantly higher than the current cost of shale gas, even taking into account the cost of liquefaction and transportation. On the other hand, the direction of significant volumes of gas for export would reduce the volume of gas in the domestic market, which would somewhat raise domestic prices at least to the level of profitability of shale gas production.

And indeed, such a simple and obvious thought, apparently, has long been in the head of the Americans. That is why in recent years they have invested heavily in the construction of liquefied natural gas facilities in the United States.

And here begins the oddities.

Potential US LNG Exports

As already mentioned, today in the world there are three main regions of natural gas consumption that import it from outside: Europe, Asia-Pacific and North America. Of course, we will not consider the potential of gas exports to Latin America or Africa due to the lack of effective demand for export gas in these regions in these regions.

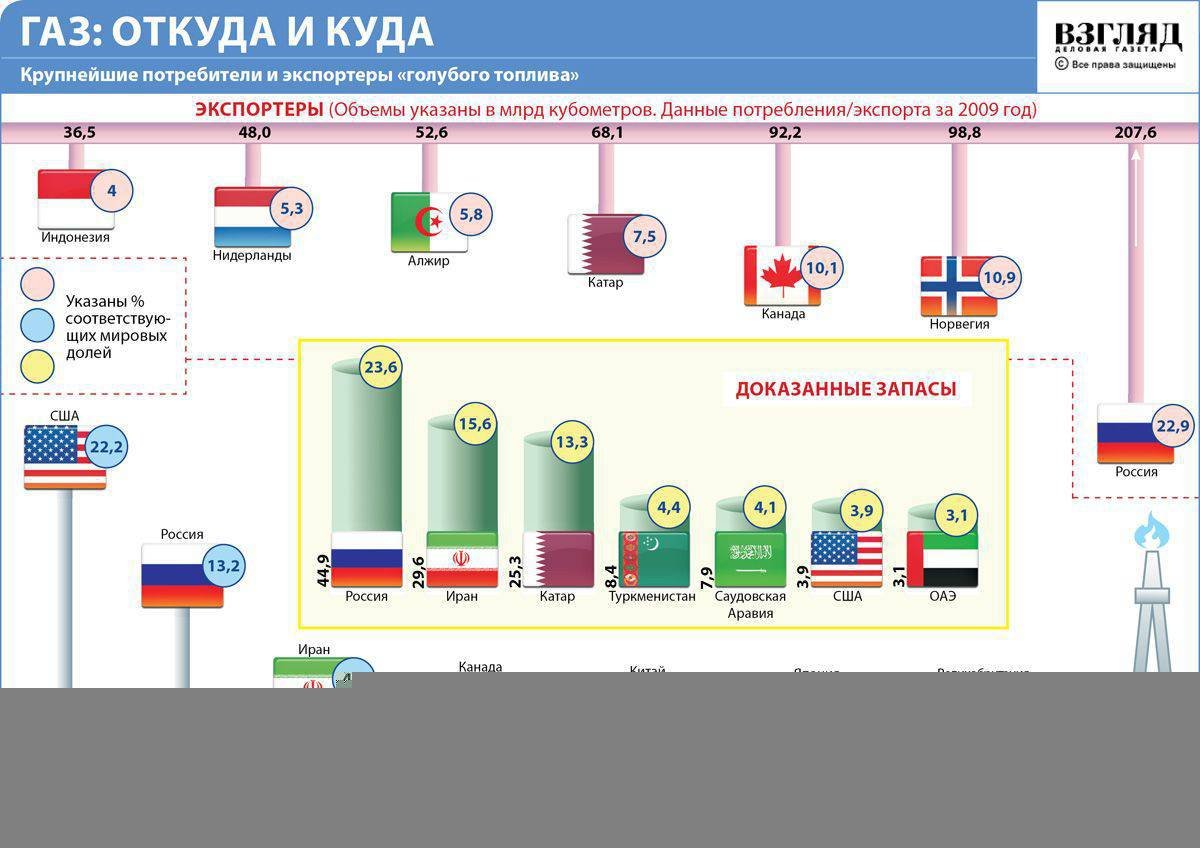

At the same time, a rather high concentration of gas exporters is observed in Europe today. In addition to Russia with its pipeline gas and gas-producing Norway, the countries of North Africa (mainly Algeria) and the Middle East (primarily Qatar) supply gas to Europe. Not averse to enter the European market and Iran, there are manufacturers from Central Asia (Turkmenistan) and Transcaucasia (Azerbaijan).

In addition, Europe is a traditional region dominated by pipeline gas from Russia (which also transports Turkmen gas), Norway, Azerbaijan and Algeria. It seems unrealistic for the US to squeeze into this market due to the previously mentioned significant excess of the cost of liquefied shale gas over the cost of pipeline gas, even despite the relatively high level of prices in Europe compared to domestic prices in the USA.

Therefore, it would seem more logical for the United States to focus on the APR market. As mentioned earlier, liquefied gas in the APR countries is almost approaching (based on the cost of one million Btu) to the price of oil: 16,6 dollars per million BTUs against 11,5 dollars per million BTUs on average in Europe.

However, in the United States, apparently, considered different. Since at present, the construction of export-oriented gas liquefaction plants has already been started, and it is being carried out on the coast of the Gulf of Mexico, where the terminals for receiving imported liquefied gas from Qatar used to be located. A simple glance at the map shows that natural gas from the coast of the Gulf of Mexico will not be transported to the APR, but to Europe.

Even without taking into account what was said earlier about higher prices for gas in the Asia-Pacific Region, this decision looks very ambiguous. Because from the point of view of transportation costs, the construction of export-oriented factories on the Pacific Coast of the USA looks more promising. Apparently, three circumstances played a role here.

Firstly, as already mentioned, today export-oriented gas liquefaction plants are located practically on the site of terminals for receiving liquefied gas previously imported to the United States. Re-equipment of such terminals, of course, is cheaper than building new factories in the open field.

Secondly, any infrastructural construction on the Pacific Coast will strategically make the United States very vulnerable to gas supplies to the APR: after building plants in the western United States, it will be much more difficult to transport gas to the east, to Europe. In the Asia-Pacific Region, Japan (US-friendly) is the main buyer today, but China is capturing an increasing share of the gas consumption market.

Get China as the main buyer of its gas the United States, apparently, not very torn. And, taking into account his own hegemonic manners, and taking into account China’s manner of twisting the hands of energy suppliers, knocking down prices as much as possible, the United States can easily be understood. Separate European satellite consumers, of course, are much more convenient than China.

Thirdly, the main area of consumption of natural gas in the United States is also located in the immediate vicinity of the Gulf of Mexico. So in the event of any change in the situation, the United States will be able to relatively easily re-equip export gas liquefaction plants back to terminals for receiving imported gas.

It would seem, what does Ukraine have to do with it?

And now we must once again return to the previously advanced thesis that there is no place to spit on the European gas market, where even without them there is no place to spit, and even with their expensive shale liquefied gas. If only one of the major suppliers of natural gas does not leave this market or if the European market becomes inaccessible for such a supplier - in whole or in part - due to any administrative barriers.

Who could potentially leave? - Well, I don’t know, maybe it could be Russia with its share in the European market around 30%?

I can be accused of conspiracy here. However, excessive gas production in the United States, where prices are several times lower than prices in Europe and the APR, is not a conspiracy, but a dry fact. Exactly the same dry fact is the construction in the USA of export-oriented gas liquefaction plants on the coast of the Gulf of Mexico, from where gas can only be transported to Europe.

If the US has gas and if the US builds the infrastructure to transport it to Europe, then it’s logical to conclude that they want to sell their gas in Europe. If someone can make some other conclusion, I will listen to it with pleasure, but for the time being I will stick to this particular hypothesis.

And for this it is necessary to press someone from the previous gas suppliers to the European market. As they say, nothing personal but business.

How can you limit gas supplies to Europe from any other country by non-market methods? - Well, first of all, introduce some administrative barriers. For example, some sanctions. The second line of action is to make high-risk deliveries from this country to Europe.

For example, because a certain transit country striving for democracy and freedom, as well as rebelling against takeovers from the country exporting gas, steals gas destined for Europe.

Ukrainian crisis and the gas issue

From the very beginning of the Ukrainian crisis, all more or less attentive observers did not leave the feeling that the United States, through its actions, was purposefully pushing Ukraine towards a financial catastrophe.

Here is the notorious European integration. Here and the internal instability that followed it, which resulted in a full-scale squabbling of oligarchic clans both in the area of internal intrigues and in the financing of various marginal groups, from titus to the Right Sector.

Here and the aggravation of anti-Russian hysteria, when to discredit Yanukovych, who postponed the issue of European integration, both the idea of the Customs Union and Russia as a whole began to be actively attacked.

Then we ourselves entered the game by joining the Crimea. Of course, in that situation it was a correct, timely and quite logical deed, but in the USA they decided to immediately use it in their own interests.

Because explaining that shaft of anti-Russian hysteria that followed in the Western media after the annexation of the Crimea, it only seems to me somewhat naive to the wounded pride of the American elite: tough pragmatists set the tone, who by and large do not care about Crimea or Ukraine. And who are anyone, but not hysterics.

One would assume that the United States is annoyed by the final loss of Crimea as a potential NATO base. However, then the tone of the Western media would be a bit different: until recently, the possibility of annexing the Crimea would be denied, any horrors that would follow for the Crimeans would be drawn, everything would be done to reject the Crimea back. In a word, there would be approximately such rhetoric that prevailed over this in the Ukrainian media.

In fact, the following happens: The West in fact acknowledged the entry of Crimea into Russia, which was repeatedly stated by the leading media. And the main focus today is not on rejecting the Crimea back, but on punishing Russia for the Crimea, which in this case is used only as a convenient excuse.

Reason for what, let's remember? Well, the States frankly said why: including in order to inflict maximum damage to Russia on the field of energy exports.

And then these are here the masterpiece statements of the IMF about the fact that Ukraine will be given a loan, provided that the gas discount remains. Just undisguised throwing of firewood on the fire.

Ukraine is bankrupt. The gas crisis there is only a matter of time, as mentioned earlier. Sanctions against Russia - the issue is resolved. If gas supply disruptions to Europe due to the inadequacy of Ukraine begin, national European governments simply cannot resist the fierce pressure of the US and the EU bureaucracy and will impose sanctions on trade flows.

The fact that, with the bankruptcy of Ukraine, gas breakdowns will inevitably begin, it seems to me such an obvious two-way process that even someone like Mr. McCain with his tired mind of a Cold War invalid could have thought of.

And here, apart from all other things, American TNCs are purely hypothetical, all are in white, and they say: But we can deliver to Europe, suffering from energy blackmail from this barbarous Russia, headed by this bloody tyrant Putin, our liquefied natural gas. Well, yes, it will be a little more expensive than buying from Russians, well, after all, the ideals of freedom, democracy and European Ukraine are even more expensive!

Of course, the Europeans, themselves no less cynical than the Americans, were hypothetically and would be happy to put on all these hypothetical American reasoning with a tremendous device. But in conditions of a full-fledged information war with Russia, they may not be able to do this.

How likely is such a scenario? From a technical point of view, it is limited only by the volume of gas production in the United States. As far as is known today, shale gas production has suspended its rapid growth, which it demonstrated in the second half of its zero years, mainly due to a sharp drop in domestic gas prices in the United States.

However, if US companies are guaranteed supplies to Europe - and they will inevitably be guaranteed in case of administrative barriers against Russia - Americans can easily increase shale gas production, even bearing significantly higher costs than today.

Moreover, the alternative to this for them personally is the continuation of the stagnation of the shale gas market in the United States, which cannot develop at current domestic prices. From an organizational point of view, it depends only on how inclined Europeans are to succumb to US pressure.

Of course, I do not claim that all events in Ukraine were started only with the aim of squeezing Russia out of the European gas market. Moreover, as I have already said, in the West there is no single center for decision-making, and therefore no single system of goals. We in the face of the West are dealing with a network consisting of various interest groups.

I just tried to highlight a small area of such a network associated with natural gas. In a word, it is unlikely that the lobbyists of US energy companies were involved in planning the crisis in Ukraine. However, the fact that they decided to use them in their interests, in my opinion, is beyond doubt.

Possible counterplay Russia

In the light of the above, the position of Russia in this particular party looks very complicated. With any succession of events, a full-fledged gas crisis is guaranteed in Russian-European relations, and in Ukrainian-Russian relations it is already underway.

I personally find it inevitable that the US energy companies will inevitably try to take advantage of the current state of affairs to enter the European gas market: I’ll not consider the hypothesis that Americans build gas liquefaction plants on the coast of the Gulf of Mexico. .

If Russia doesn’t do anything in this direction, but simply goes with the flow, predictably responding to the “don’t give money - turn off the gas” scenario, then the keys to implementing such a scenario are completely in the hands of our respected European and American partners.

How these keys are used will depend on their internal bargaining, but not on us. As in the case of overlapping only gas supplies to Ukraine (which immediately begins to steal European gas), and in the event of the cessation of both supplies to Ukraine and transit through Ukraine to Europe, we give the supporters of the above actions the whole set of arguments to justify them.

The only way out in this particular game is maneuvering of the following nature. Today, the States are actively trying to tie Europe with sanctions against Russia.

Russia, for its part, needs to tie Europe with a joint solution of the gas issue with Ukraine. Unfortunately, it is already clear that Europe will not pay instead of Ukraine or credit Ukraine for these purposes.

Similarly, it is clear that the IMF in this area pursues opposite - pro-American - goals. Accordingly, the only narrow space for maneuvers in Russia remains some variant of subsidizing Ukraine in terms of its gas purchases against any joint guarantees of Ukraine and Europe.

By the way, we tried to turn it around, promising Yanukovych at the time loans from the National Welfare Fund, including for the purchase of gas. Or does someone think that we did it out of the goodness of our heart? - No, just the gas crisis is not just unprofitable for us today, it is strategically dangerous for us.

That our counterplay was refuted at the end of February when Yanukovych was overthrown. Today it is necessary to urgently find the possibility of alternative counterplay. In the gas issue, we now more than ever need a cold head. An impulsive attempt to chop off the shoulder may cost us not short-term failures of European supplies, but a complete or partial loss of the main European market for us.

Information