The impact of the Customs Union on the economy of Kazakhstan

The economy of Kazakhstan has been operating for more than two years under the conditions of the Customs Union. Around this very important for all countries of the participants of the association there are constantly disputes about the benefits and profits for different countries. Unfortunately, good analytical materials supported by statistics are rare. Partly, this post appeared precisely because I could not find enough quantitative data on the results of the activities of the customs union, partly as a desire to express my opinion on economic integration with Russia and Belarus.

The economy of Kazakhstan has been operating for more than two years under the conditions of the Customs Union. Around this very important for all countries of the participants of the association there are constantly disputes about the benefits and profits for different countries. Unfortunately, good analytical materials supported by statistics are rare. Partly, this post appeared precisely because I could not find enough quantitative data on the results of the activities of the customs union, partly as a desire to express my opinion on economic integration with Russia and Belarus.In this post we will try to answer such questions:

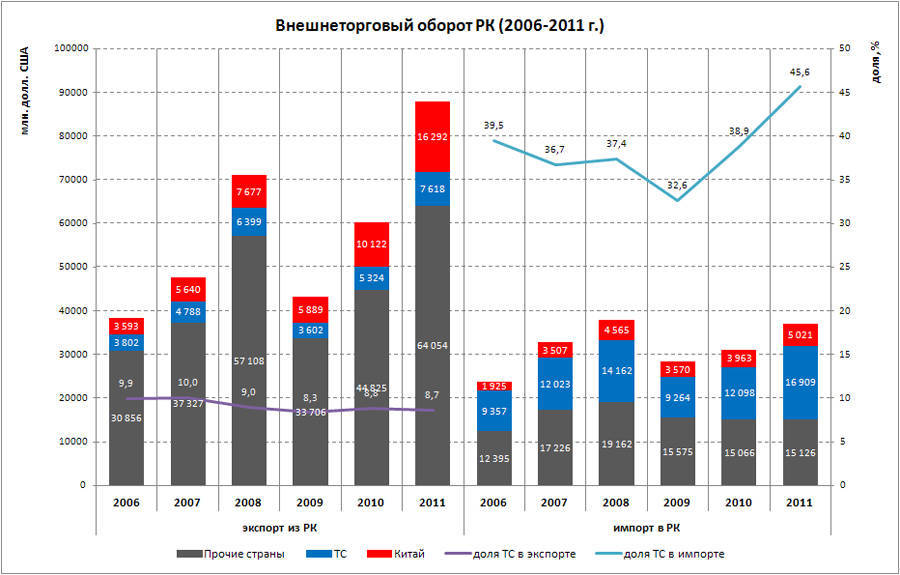

Dynamics of foreign trade turnover of Kazakhstan

One of the main tasks of the creation of the customs union was the desire to increase trade and export of Kazakhstan goods to the CU countries. Consider the data of the Customs Committee of Kazakhstan on the volume of foreign trade of Kazakhstan and trade within the CU.

The graph shows that the largest decline in foreign trade occurred in 2009, the year of greatest recession after the economic crisis. Since 2010, there has been a steady increase in international trade both in the CU countries and in other countries of the world.

The share of imports of goods to Kazakhstan in total trade with the CU countries is about 70%. By and large, we are much more “giving away” to the economies of Russia and Belarus than “helping out” from the sale of our goods in these countries. At the same time, the union is, of course, the main partner of the Russian Federation. The Russian Federation occupies about 97% in the trade turnover of Kazakhstan with the CU countries; Belarus, respectively, only 3%.

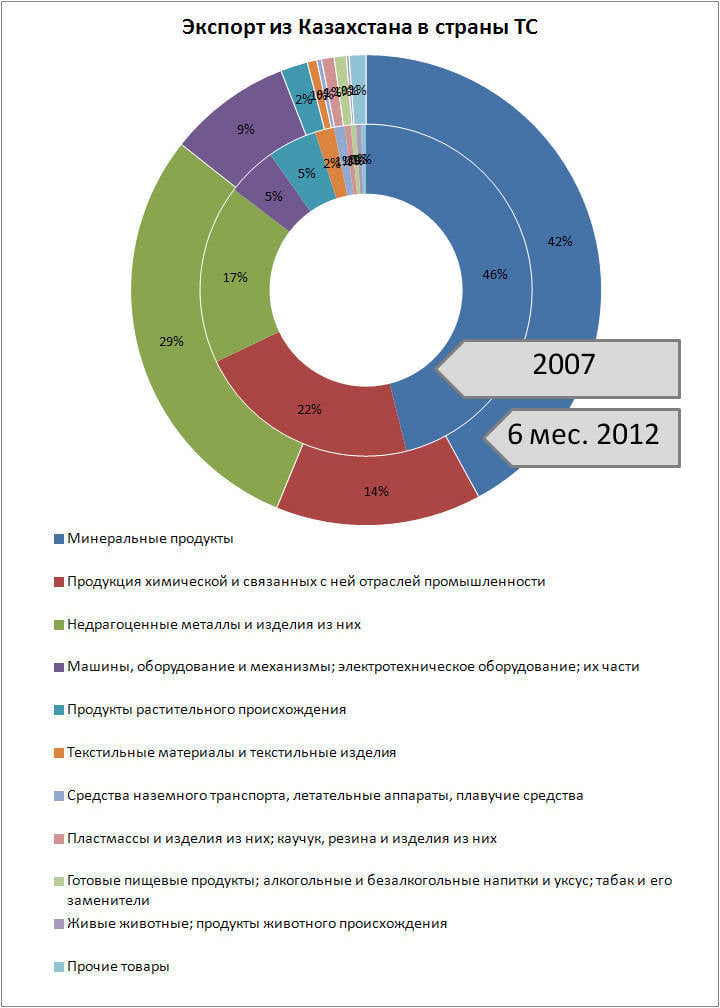

Commodity structure of trade with the countries of the Customs Union

If we consider the structure of the entire foreign trade of Kazakhstan (with all countries), then the influence of the CU becomes noticeably strong. Thus, in total exports from Kazakhstan, the share of exports to the CU countries from 2008 of the year tends to decrease (for example, in 2007, exports to Russia and Belarus occupied about 10% of total exports from Kazakhstan, and in 2011, only 8,7%). This indicates that since the beginning of the CU operation, our trade policy towards Russia and Belarus did not undergo fundamental changes: as we exported there about 9% of our exports before the CU was established, we also export them later. The growth of exports from Kazakhstan to the countries of the Customs Union is only partially explained by the reasons for creating the CU, the main reasons, in my opinion, are the same mechanisms that ensured the growth of all Kazakhstani exports (revitalization of the world economy, favorable conjuncture in commodity markets).

The situation is quite different with the import of goods from Russia and Belarus to Kazakhstan. Immediately after the creation of the CU, imports to Kazakhstan from Russia began to increase dramatically. So if in 2007, imports from Russia accounted for about 36,7% of the total imports to Kazakhstan, then in 2011, it became almost 46%. Those. Kazakhstan’s imports have become even more supplied with goods from Russia.

Conclusion: With an obvious increase in commodity turnover within the framework of the customs union, its creation did not greatly change the position of Russia and Belarus in the export structure of Kazakhstan, but rather strongly affected the structure of imports to Kazakhstan. Kazakhstani imports became even more supplied with goods from Russia.

The commodity structure of exports from Kazakhstan has changed, but not drastically. The leading position still belongs to mineral products (ie, raw materials: primarily oil products, ores and concentrates). Kazakhstan's chemical and metallurgical products are also popular in Russia and Belarus. Also noteworthy is the increase in the share in exports of such a group as computing equipment. True, to be honest, I am confused by this article, because in Kazakhstan, sufficiently well-developed industrial productions of computing equipment have not yet been observed. Those. By and large, there are no fundamental changes in exports from Kazakhstan to the CU.

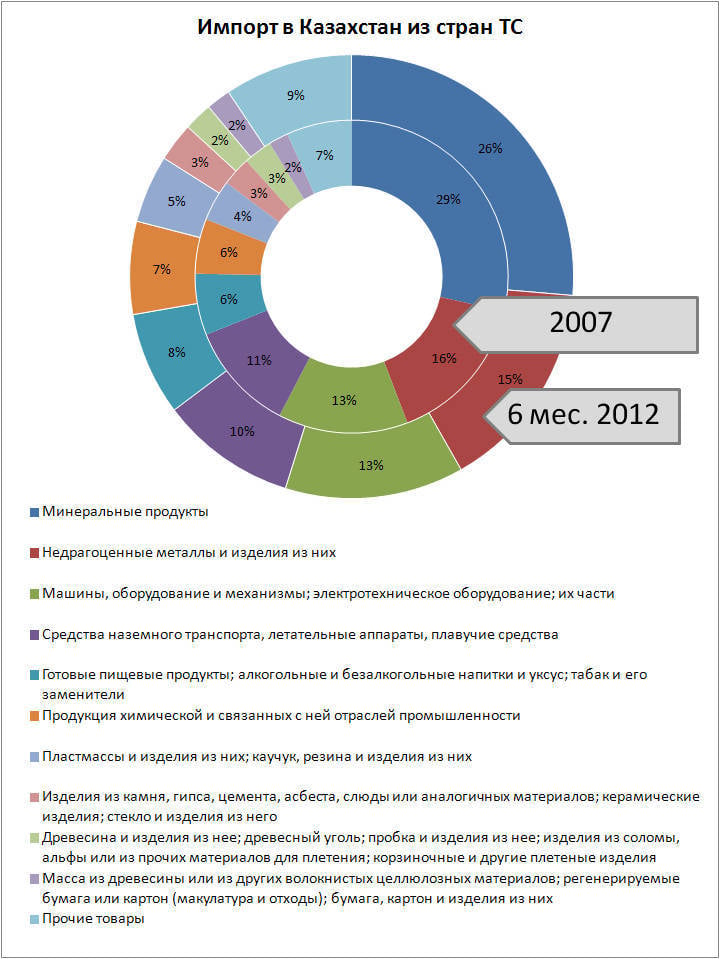

There are no significant changes in the structure of imports to Kazakhstan.

As before, mineral products (oil and oil products, ores and concentrates, coke, etc.) are leading in imports from Russia - 26%.

In second place is a large group - metallurgical products (metal, pipes, rods, and much more). This group accumulated in 2012 about 15%. 13% of imports is a group of machines and equipment. The fourth place belongs to the group “Vehicles” - 10%. And 8% comes from ready-made foods.

The conclusion from the graphs above can be made as follows: Approximately the same goods and in the same proportion as before the creation of the customs union are exported to Kazakhstan from the CU countries.

It should also be noted that the export operations of Kazakhstan primarily include raw materials and industrial goods, i.e. Benefit from the creation of the vehicle and simplify the movement of goods will receive, first of all, the major Kazakhstani industrial producers (in the areas of oil and gas, metallurgy, mining, chemical industry). Unfortunately, the change in the structure of Kazakhstan's exports in the direction of consumer goods has yet to be said.

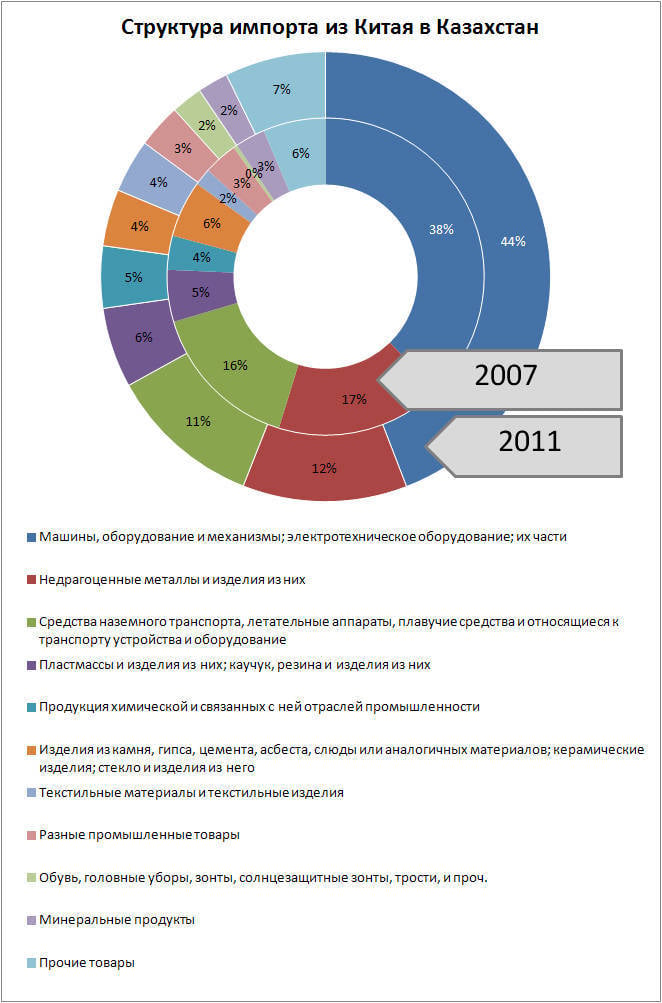

China's trading activity towards Kazakhstan

Another task was to limit imports of goods from China, but according to the Customs Committee, trade with China only slightly slowed down its growth in 2010, but in 2011 it had already surpassed its pre-crisis maximum.

The structure of import of goods from China before and after the creation of the customs union also remained almost unchanged. China is still active in the import of various machinery and equipment, non-precious metals and products from them (metal, pipes, rods, etc.), vehicles, plastics, plastic products, textiles, shoes and many other things.

Conclusion: the creation of the CU did not significantly affect the foreign trade activity of China in relation to Kazakhstan.

It was statistics, and statistics is a stubborn thing.

Pros and cons of the creation of the Customs Union

Further, I would like to consider the main pros and cons of creating a customs union for Kazakhstan, and finally understand, for the benefit of Kazakhstan, the customs union or to the detriment.

Pros:

Cons:

In my opinion, in the strategic aspect, such integration will be very useful, and is a natural continuation of the already close cooperation with Russia. It would be foolish to reject the fact that during all the years of independence we have been actively working with Russia, which is one of the main partners of Kazakhstan, not only in trade, but also in many other areas. Russia is much closer to Kazakhstan than, for example, the other strongest player in the region, China. And it is quite natural that the idea of such a union arose with Russia, and not with China.

In macroeconomic terms, the vehicle also has more advantages than minuses, since we have a more simplified variant of transit and sale of our main goods (oil, raw materials, grain, etc.) to the main consumers (EU, Russia).

After the transition period, when the rules of doing business in the new environment will be shaped, the investment attractiveness of creating new joint ventures will increase significantly. Kazakhstan is more attractive in terms of setting up and running a business, so one should expect that our country will be more attractive to foreign investors. A clear example is the recent visit to Kazakhstan and the agreements reached with representatives from Vietnam.

But there are problems and disadvantages of integration. They must not be forgotten, they must be recognized, they must be worked with. Many of the negative aspects associated with the activities of the CU arise from the breakdown of the old mechanisms of work and the incompleteness, and often the lack of new mechanisms. Such problems are inherent in any transition period. In my opinion, a similar period can last even 3-5 years before a relatively workable set of documents, principles and standards is created allowing to effectively solve the tasks set for the union.

Another important drawback is the threat of a decrease in the competitiveness of Kazakhstani goods in relation to Belarus and Russia. Such an increase in competition can be viewed from two opposite aspects. I agree that it will become more difficult for Kazakhstani businessmen to work in some markets, but on the other hand, the growth of competition will force Kazakhstani businessmen to improve their business processes. As shows story economy, competition brings more advantages than disadvantages and is the driving force of progress. First of all, consumers benefit from competition.

It should also be borne in mind that the Kazakh market is not so capacious that Russian commodity producers rush to it in orderly rows. We are interested in Russian partners, primarily as consumers of industrial goods (machinery, equipment, consumables for the mining, oil and gas, agriculture and other industries) and as a major supplier of raw materials. This is also evident in the structure of imports and exports with Russia and Belarus.

The rise in prices is one more minus, actively discussed in the press. It is based on two main trends: a rise in prices for goods from third countries due to the increase in customs tariffs; The second trend is speculation at lower prices in Kazakhstan compared to Russia. Regarding the first trend, the average tariff rate for the republic increased by 4.4%. This is not a critical increase in the customs tariff and it is impossible to talk about a large-scale increase in domestic prices because of this.

If we consider the second upward trend in prices from Kazakhstani producers, on the contrary, it is positive for them. Some of our products are cheaper than Russian ones, which means that our manufacturers have a real competitive advantage over Russian or Belarusian ones. Here again, it is clear that the customs union provides advantages for local producers, when Russian buyers can purchase most of their products. I think no one will argue that for sellers such an expansion of sales opportunities is very profitable. On the other hand, local consumers suffer because the law of supply and demand aligns our prices with Russian.

Therefore, it cannot be said that such an alignment is an absolute evil for Kazakhstan, producers benefit, consumers suffer. In general, public statements on this issue look illogical, on the one hand they care about the problems of our manufacturers, that they suffer from the creation of the CU, but as soon as some local players, according to the law of supply and demand, level up (in this case, increase) their prices, they come out to new Russian buyers, and thereby win, everyone starts to swear and be indignant about this situation. We need to be completely honest, if we want to support our producers, it means that we need to create conditions for them when they can get enough profit for development, which means being ready to buy lower-quality Kazakhstani goods, at higher prices and give them the opportunity to earn money. selling goods to Russia (and thereby reducing the domestic supply of goods, which causes a rise in domestic prices).

In general, I look at the integration processes with Russia positively. Our economies are already rather intertwined, integration is quite natural. In macroeconomic terms, Kazakhstan gets more than it loses. First of all, the large industrial enterprises of Kazakhstan benefit (Oil and gas, mining, metallurgy, chemical industry, etc.). The main disadvantages and problems arising from the creation of the CU stem from: deficiencies or the lack of new mechanisms; now there is a transition period; due to insufficient competitiveness of some of our products and problems in price regulation. In my opinion, we need to recognize these problems, work with them and gradually come to effective mechanisms for the functioning of the union.

Information